Can You Actually Afford to Buy in Tarneit — Or Are You Guessing?

You may only need ~5% deposit to buy in Tarneit. See your exact numbers in minutes).

Takes 2 minutes • No credit check • No obligation

You leave with a clear buying plan.

Fast Affordibility Snapshot

What Buying in Tarneit Could Look Like

(Example with typical Tarneit house price)

Example Price

$660,000

Deposit (5%)

$33,000

Estimated Repayment

~$3,631/month

Typical Household Income required

~$100K–$130K combined

This is based on a typical dual-income household. Your numbers may be different depending on your income, debts, and lender criteria.

Why Most First Home Buyers Get This Wrong

Online calculators often give false confidence — banks assess your income very differently

Many buyers either overestimate or underestimate what they can afford

Deposit isn’t the only cost- repayments and borrowing limits matter more

Waiting for “perfect timing” often costs more than acting with clarity

Free 10-minute strategy call. No obligation.

Should You Buy or Build in Tarneit?

Tarneit is one of the few suburbs where first home buyers still have both options:

Buying Established

Move in sooner

Less uncertainty

Easier processBuilding New

Lower upfront cost in some cases

Government incentives may apply

More flexibility in design.The right choice depends on your borrowing power, timeline, and risk tolerance — not just price

Takes 2 minutes • No credit check • No obligation

Is this Right for you?

You can own a home in Tarneit if:

✔ You are a first home buyer

✔ You have around $30K–$70K saved for deposit

✔ Your household income is roughly $100K+

✔ You are looking at homes around $600K–$700K

What Upfront Costs Should You Expect?

Beyond your deposit, most buyers need to budget for:

• Conveyancing: ~$1,200

• Building & pest inspection: ~$600–$750

• Other costs (e.g. movers): ~$800–$1,500Stamp Duty (Victoria):

$0 up to $600K (eligible first home buyers)

Concessions available up to $750K

These costs vary based on your situation and eligibility.

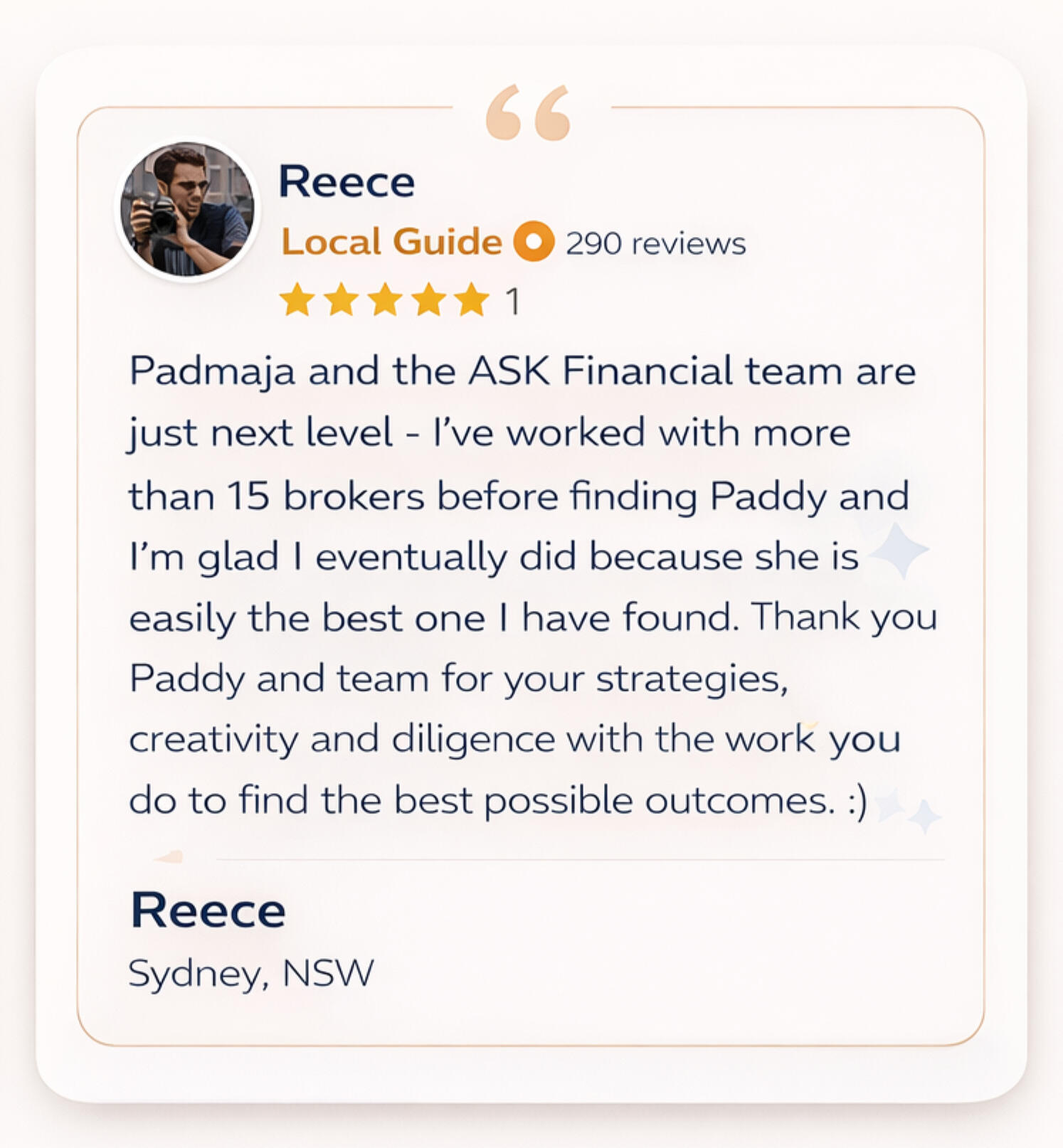

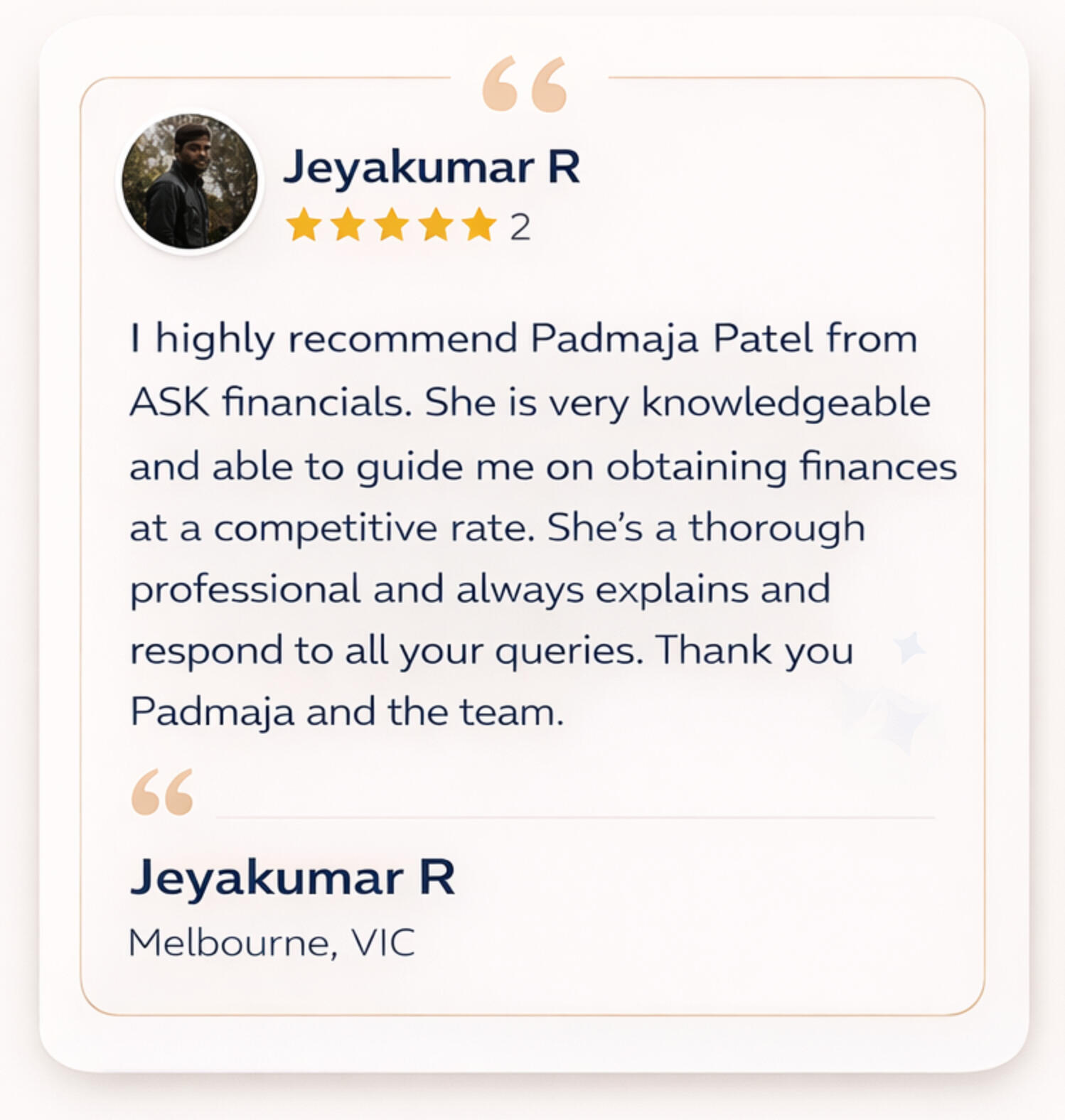

What First Home Buyers Say About Working With Us

Trusted by first home buyers across Melbourne

⭐ 5-Star Rated Mortgage Broker

Helping first home buyers secure homes with clarity and confidence

Ready to See If You Can Buy in Tarneit?

Get a clear plan based on your income, deposit, and borrowing power.

✓ Understand exactly how much you can borrow

✓ See your real repayment range

✓ Get a step-by-step plan to buy your first home

Free 10-minute clarity call — no pressure, no obligation

What Happens Next

A simple, guided process - no pressure, no confusion

A simple, guided process - no pressure, no confusion

Most buyers I speak to are either overestimating or underestimating what they can afford — both can cost you the right property.

Padmaja Patel

I help first home buyers across Melbourne and Victoria understand exactly what they can afford — before they commit to a property.

Can First Home Buyers Afford to Buy in Tarneit?

These are the most commonly asked questions by my first home buyer clients.

How much deposit do I need to buy a house in Tarneit?

Most first home buyers in Tarneit purchase with around a 5% deposit, which can be approximately $30,000–$40,000 depending on the property price. Government schemes may allow eligible buyers to purchase with a low deposit and avoid LMI.

How much income do I need to buy a house in Tarneit?

The income required depends on your loan amount, expenses, and debts. As a guide, many first home buyers purchasing around $600K–$700K may need a combined household income of $100K–$130K, but this varies based on your situation and lender assessment.

How much are repayments on a $600K–$700K home loan?

Repayments will depend on your interest rate and loan size. As a rough guide, a loan around $600K–$650K may have repayments of approximately $3,500–$4,000 per month at current interest rates. Your exact repayments will vary.

What upfront costs do I need to budget for when buying in Tarneit?

In addition to your deposit, typical upfront costs include:- Conveyancing: approximately $1,200

- Building and pest inspection: approximately $600–$750

- Moving and setup costs: approximately $800–$1,500Eligible first home buyers in Victoria may pay no stamp duty up to $600K, with concessions up to $750K.

Can I buy a home with a 5% deposit in Victoria?

Yes — many first home buyers purchase with a 5% deposit using government support schemes or lender options. These programs can help you enter the market sooner with lower upfront costs.

Is it better to buy or build in Tarneit?

Tarneit is popular for both buying established homes and building new homes.Buying established = faster move-in

Building = more choice and potentially lower upfront costThe right option depends on your timeline, budget, and borrowing capacity.

How do I know how much I can borrow?

Your borrowing capacity depends on:- income

- existing debts

- living expenses

- interest rate buffersBanks assess all of these factors — not just your salary — to determine how much you can borrow

What is the first step to buying a home in Tarneit?

The first step is understanding your borrowing capacity and budget before looking at properties. This helps you avoid overestimating or underestimating what you can afford and ensures you search within the right price range.

Still unsure how much you can borrow or what you can afford in Tarneit?

Get your personalised borrowing plan based on your income and deposit.

Free 10-minute clarity call — no pressure, no obligation

Padmaja Patel - Mortgage Brokers ABN: 17153479338. Credit Representative # 562032 is authorised under Australian Credit License #389087.Disclaimer: This page provides general information only and has been prepared without taking into account your objectives, financial situation or needs. We recommend that you consider whether it is appropriate for your circumstances and your full financial situation will need to be reviewed prior to acceptance of any offer or product. It does not constitute legal, tax or financial advice and you should always seek professional advice in relation to your individual circumstances.

Text